Money Deals 2026: Best Financial Deals to Save More, Earn More & Build Real Wealth

In 2026, the smartest financial move isn’t just about what you earn — it’s about what deals you find. From high-yield savings accounts paying 5%+ to credit card cashback worth hundreds of dollars a year, the money deals landscape has never been richer. This complete guide covers every category of financial deal available right now, with real data, honest comparisons, and a step-by-step strategy for getting the maximum value from every dollar you save or invest.

Key statistics — money deals in 2026

| Metric | Figure |

| Average annual saving per household using money deals | $1,800 |

| Top high-yield savings APY available (2026) | 5.3% |

| US fintech market value | $600 billion+ |

| Adults who say finding a better financial deal is a priority | 73% |

| More interest earned: high-yield vs standard savings | 3.2× |

What are money deals — and why do they matter more in 2026?

Money deals are promotions, bonuses, preferential rates, and financial incentives offered by banks, fintech platforms, investment apps, and credit providers to attract or retain customers. They span every area of personal finance — from the interest rate on your savings account to the cashback on your credit card, from the sign-up bonus on your investment app to the fee waiver on your mortgage.

They matter more in 2026 because competition between financial providers has never been fiercer. Traditional banks are fighting fintech challengers for deposits. Investment platforms are slashing commissions to zero. Insurance providers are offering switching bonuses. The net result is an unprecedented level of deal availability — but only for people who actively seek them out.

The average household that actively uses financial deals saves $1,200–$2,400 per year compared to those who stay with default products. Over 10 years, compounded, that difference is the equivalent of a first-time home deposit contribution.

Average annual benefit of actively using money deals by category:

| Deal category | Annual benefit |

| Credit card cashback | $480 |

| Mortgage rate deal | $420 |

| High-yield savings | $390 |

| Loan rate reduction | $320 |

| Investment platform bonuses | $280 |

| Bank switching bonus | $200 |

| Insurance switching | $180 |

The 7 types of money deals — complete guide

- High-yield savings account deals — highest impact for most people

A high-yield savings account (HYSA) pays significantly more interest than a standard bank savings account. In 2026, the best HYSAs pay 4.8–5.3% APY compared to 0.4–0.6% at major traditional banks. On a $10,000 balance, that’s the difference between earning $50 per year and earning $530 per year.

- Credit card cashback and rewards deals

The best cashback credit cards in 2026 return 2–5% on every purchase, with elevated rates (up to 6%) in specific categories like groceries and petrol. Sign-up bonuses of $200–$600 are standard for premium cards.

- Investment platform sign-up bonuses

Most major investment platforms offer new account bonuses ranging from free stocks worth $10–$1,000 to commission-free trading for a set period. These deals are effectively free money for people who were going to invest anyway.

- Bank switching bonuses — 2026 trend

Switching bonuses of $200–$500 for moving your primary bank account to a new provider are now mainstream. Banks have determined that acquiring a primary bank account customer is worth paying for. For consumers, this means earning $200–$500 every 12–24 months simply by switching.

- Mortgage and loan rate deals

Even a 0.25% interest rate reduction on a $300,000 mortgage saves approximately $750 per year — $22,500 over a 30-year loan. Refinancing deals, introductory rate offers, and broker cashback schemes make this one of the highest-value financial deal categories.

- Insurance switching deals

Car, home, and health insurance providers routinely offer new-customer discounts of 10–20% compared to renewal rates for existing customers. Switching annually generates consistent savings without reducing family savings deals.

- Robo-advisor and managed fund fee deals

Fee-free periods, reduced management expense ratios, and automated investing bonuses from robo-advisors provide compounding advantages. On a $50,000 portfolio, a 0.5% fee reduction saves $250 per year — adding thousands to your final balance over 20 years with compounding.

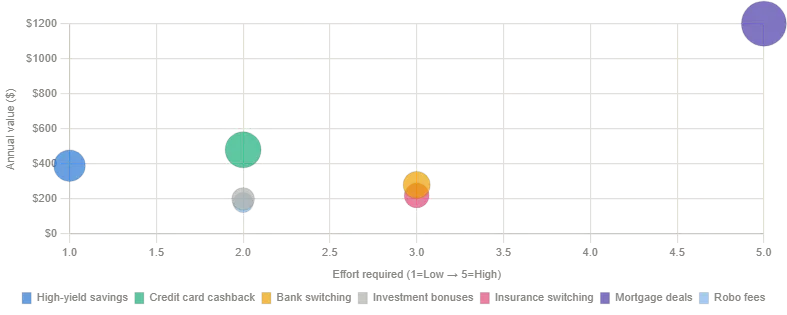

Money deals comparison — all 7 types at a glance

| Deal type | Typical annual value | Effort required | Best platform (2026) | Renewal frequency | Who benefits most |

| High-yield savings | $300–$530/yr per $10K | Low | Marcus, Ally, SoFi | Ongoing | Everyone with savings |

| Credit card cashback | $480–$900/yr | Low | Chase Sapphire, Amex Blue | Ongoing | Regular spenders |

| Investment bonuses | $50–$1,000 one-off | Low | Robinhood, Webull, Fidelity | Every 1–2 years | New investors |

| Bank switching bonuses | $200–$500 one-off | Medium | Chase, Citi, SoFi | Every 12–24 months | Anyone with direct deposit |

| Mortgage rate deals | $750–$3,000/yr | High | Rocket Mortgage, Better.com | Every 2–5 years | Homeowners |

| Insurance switching | $180–$600/yr | Medium | Policygenius, NerdWallet | Annually | Car + home owners |

| Robo-advisor fee deals | $150–$500/yr | Low | Betterment, Wealthfront | Every 1–3 years | Long-term investors |

High-yield savings vs standard savings — the real numbers

| Balance | Standard bank APY (0.46%) | High-yield APY (5.1%) | Annual difference | 10-year difference (compounded) |

| $1,000 | $4.60 | $51.00 | +$46.40 | +$638 |

| $5,000 | $23.00 | $255.00 | +$232.00 | +$3,190 |

| $10,000 | $46.00 | $510.00 | +$464.00 | +$6,380 |

| $25,000 | $115.00 | $1,275.00 | +$1,160.00 | +$15,950 |

| $50,000 | $230.00 | $2,550.00 | +$2,320.00 | +$31,900 |

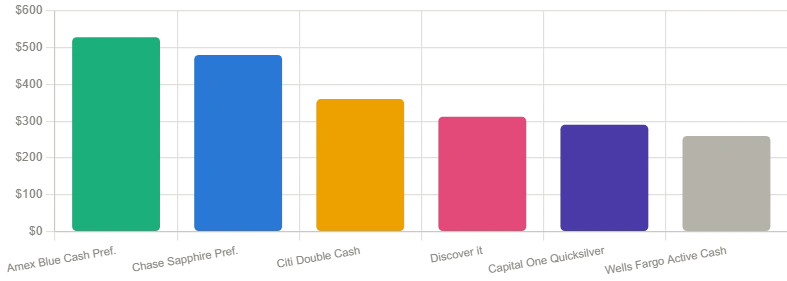

Best cashback credit cards 2026 — annual reward value

| Card | Annual cashback value | Best category | Sign-up bonus |

| Amex Blue Cash Preferred | $528 | Groceries (6%) | $300 after $3K spend |

| Chase Sapphire Preferred | $480 | Dining + travel (3×) | $750 travel value |

| Citi Double Cash | $360 | Everything (2%) | $200 after $1.5K spend |

| Discover it | $312 | Rotating categories (5%) | First year matched |

| Capital One Quicksilver | $290 | Everything (1.5%) | $200 after $500 spend |

| Wells Fargo Active Cash | $260 | Everything (2%) | $200 after $1K spend |

The 10-step money deals strategy for 2026

The 10-step money deals strategy for 2026

- Audit your current financial products first — List every account, card, loan, and insurance policy. Write your current rate or fee next to each.

- Move idle savings to a high-yield account immediately — If you have $10,000+ earning 0.5%, moving to a 5%+ HYSA earns $450 more per year with zero additional risk.

- Match your credit card to your biggest spending category — Most households leave $200–$400 per year on the table by using a generic 1.5% flat-rate card.

- Capture one bank switching bonus per year — Set a calendar reminder every 12 months to check for $200–$500 switching bonuses.

- Open an investment platform with a sign-up bonus — Free stocks or cash bonuses of $50–$1,000 are available for Professional accounts you’d be opening anyway.

- Refinance your mortgage when rates drop 0.5%+ below your current rate — The break-even period is typically 3–5 years.

- Compare insurance annually — never auto-renew — Always get 3 competing quotes before renewing any insurance policy.

- Use a cashback shopping portal for all online purchases — Rakuten, TopCashback, and Honey generate 2–15% cashback on participating retailers.

- Maximise tax-advantaged accounts before taxable investments — A 401(k), IRA, or HSA contribution reduces tax liability — a guaranteed return no market investment can match.

- Review your deal strategy every 6 months — Financial deals change constantly. A biannual calendar reminder captures 80% of available value.

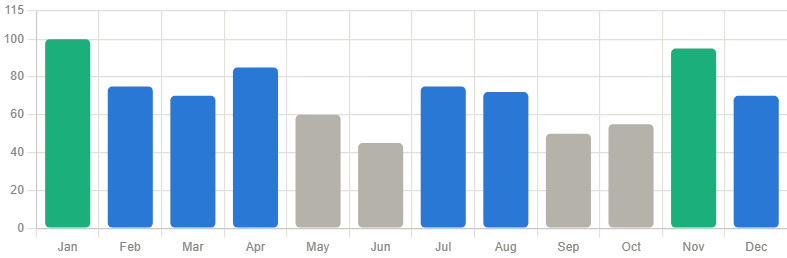

Financial deals calendar — best times to find the biggest offers

| Month / Period | Best deal type | Why | Typical deal value |

| January | Bank switching + HYSA | Banks compete for New Year budget planners | $200–$500 cash bonus |

| February–March | Tax refund investment deals | Platforms target tax refund recipients | Free stocks + bonus cash |

| April | IRA season deals | Year-end contribution deadlines | Fee-free periods, bonus interest |

| May–June | Mortgage refinancing | Spring buying season drives competition | Rate reductions + cashback |

| July–August | Credit card sign-up bonuses | Issuers push Q3 acquisition targets | $200–$750 sign-up bonuses |

| September–October | Insurance comparison | Pre-renewal season — best time to switch | 10–25% premium reduction |

| November | Investment platform deals | Black Friday extends to financial platforms | Fee waivers + stock bonuses |

| December | Year-end tax loss harvesting | Final push for tax optimisation | Tax savings + rate promos |

Top fintech platforms and their best money deals (2026)

| Platform | Deal type | Key offer | Best for | Notable feature |

| SoFi | Banking + investing | 4.6% APY + $300 bonus | All-in-one users | No account fees |

| Marcus (Goldman Sachs) | High-yield savings | 5.0% APY, no minimum | Pure savers | Goldman Sachs backing |

| Robinhood | Investment + banking | Free stock + 5% cash card | Young investors | Commission-free trading |

| Betterment | Robo-advisor | Up to 1 yr fee-free + 5.5% cash | Passive investors | Auto tax-loss harvesting |

| Chime | Banking | $100 friend referral bonus | Fee-haters | Early paycheck (2 days) |

| Wealthfront | Robo-advisor + banking | 5.0% APY cash account | High earners | Automated index investing |

| Acorns | Micro-investing | $20 bonus first investment | Beginners | Round-up investing |

Common money deal myths — busted

“Chasing deals damages your credit score” Mostly false. Opening a new credit card creates a small temporary score dip of 2–5 points but also increases total available credit, improving your utilisation ratio — often resulting in a net score improvement within 3–6 months.

“High-yield savings accounts are risky” False. FDIC-insured HYSAs carry the same $250,000 per-depositor federal deposit protection as traditional banks. The interest rate is higher; the risk is identical.

“Bank switching bonuses have too many conditions” False in most cases. The typical requirement is direct deposit of $500–$1,000 for 60–90 days — zero effort for employed people with regular payroll deposits.

“You need to be wealthy to benefit from financial deals” False. Many of the best deals — bank switching bonuses, cashback cards, investment bonuses — have no minimum balance requirements. A household with $5,000 in savings can generate $600–$900 per year in financial deal benefits.

Frequently asked questions

What is the best money deal available right now in 2026? For most people, switching idle savings to a high-yield savings account paying 4.6–5.3% APY. It requires no ongoing behaviour change, carries no additional risk (FDIC insured), and generates hundreds of dollars per year in additional interest.

How do I find the best money deals without getting overwhelmed? Focus on one category at a time. Start with savings (highest impact, lowest effort), then credit cards, then insurance. Use comparison sites like NerdWallet, Bankrate, and CountDeals to shortlist options.

Are money deals from fintech companies safe? FDIC-insured accounts at fintech banks carry the same $250,000 per-depositor federal deposit protection as traditional banks. Always verify FDIC membership before depositing funds.

Can I use multiple money deals at the same time? Yes — and you should. Stacking deals across categories (HYSA, cashback card, switching bonus, investment bonus) is completely legitimate and the approach used by financially savvy consumers.

What is the difference between APY and APR? APY (Annual Percentage Yield) accounts for compound interest. APR (Annual Percentage Rate) does not. For savings accounts, always compare APY. For loans and credit cards, compare APR.

How much can I realistically save per year using money deals? A household actively using 4–5 deal types can realistically save $1,200–$2,400 per year. Those with larger balances, mortgages, or higher spending will benefit more. The key variable is effort — reviewing deals twice a year consistently outperforms set-and-forget.